The Battle of the Flywheels

The Battle of the Flywheels

A synopsis of Curve Finance's incentives and interactions with the ecosystem's protocols, better known as "The Flywheel"

This is a component of the larger writeup on Convex Finance, linked here!

FLYWHEELS

Creating deep, efficient liquidity in crypto is highly reliant upon the yield that a Liquidity Provider (LP) can obtain by deploying capital. A common method for getting users to contribute their assets is by giving them some of your token while they’re LPs. This is done by either distributing or inflating the protocol’s own tokens, causing sell pressure, and then when the faucet turns off, liquidity dries up and moves on. Additionally, a stablecoin wouldn’t be able to print to infinity without breaking the coveted, necessary peg. So what can be done?

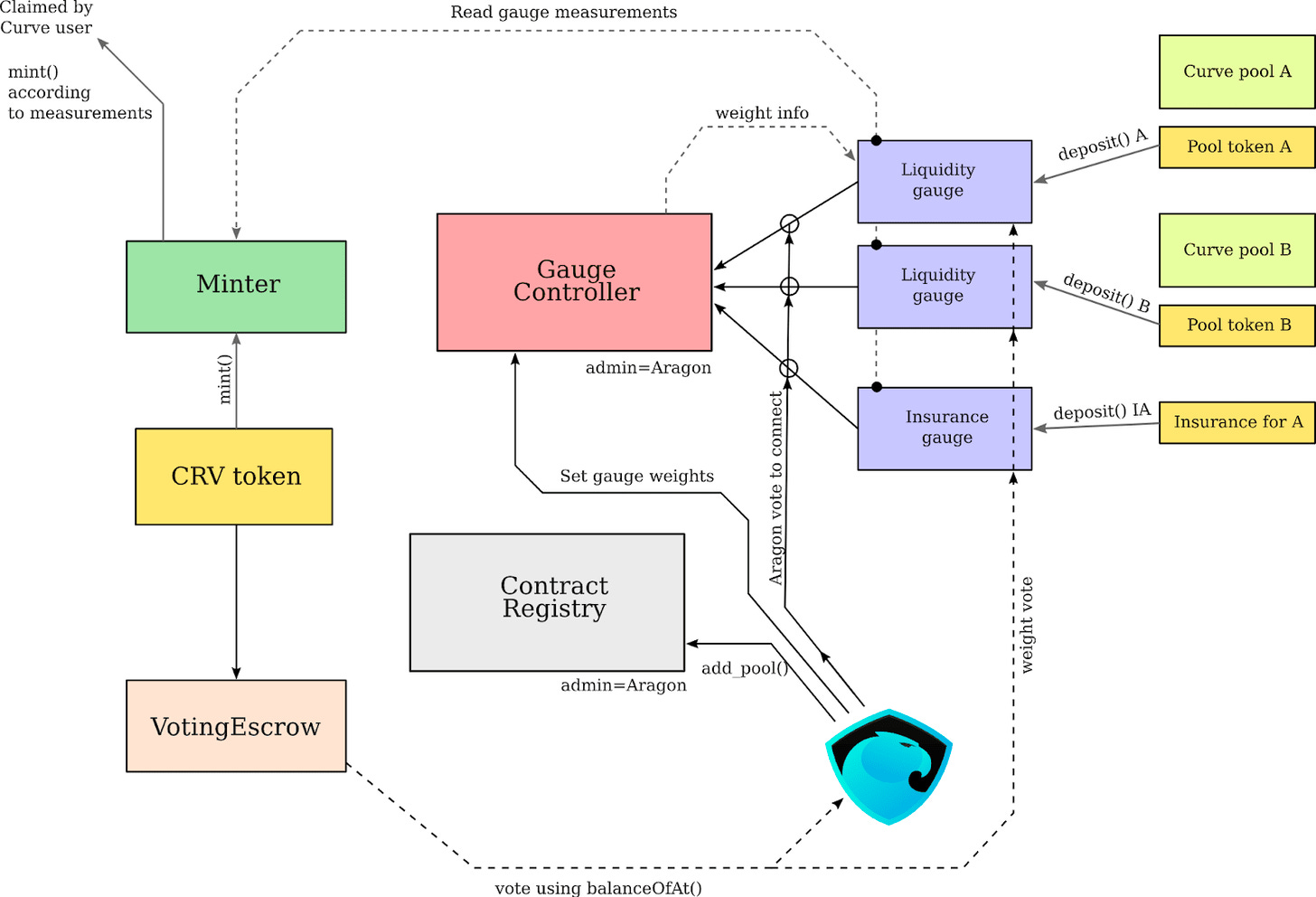

This protects the value of the token pairs, minimizes Impermanent Loss (IL) caused by one constantly inflating, and also distributes Curve’s governance power in a highly decentralized manner. Curve issues their protocol token (CRV) which is then converted into veCRV, the governance & voting token, defining the CRV rewards for the next epoch. More CRV (locked into veCRV), more yields in CRV, more CRV, and so on. Welcome to the Flywheel.

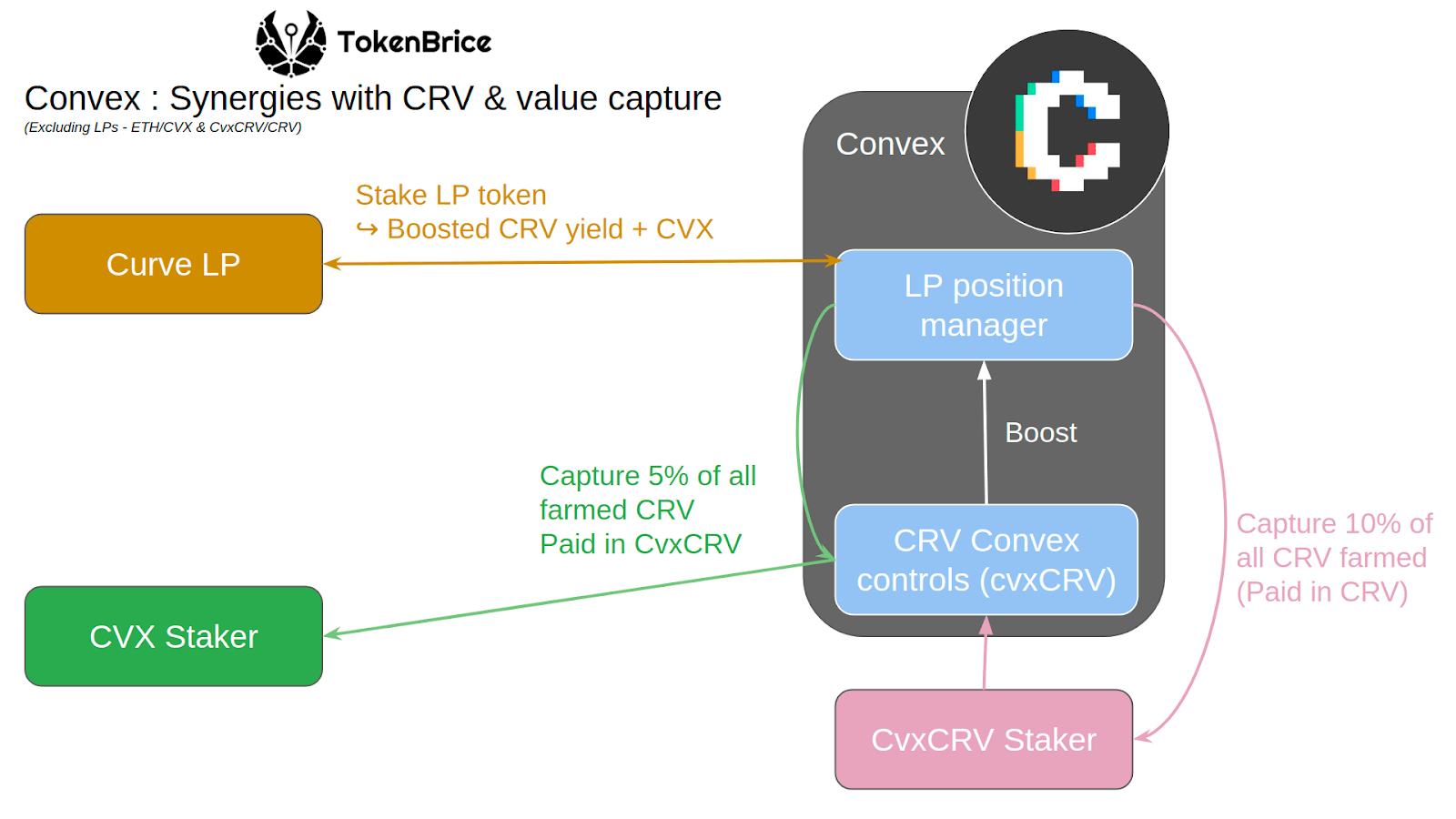

Now, add in a protocol like Convex where you can lock your earned CRV, get a healthy yield in both locked CRV (cvxCRV) and CVX, which allows you to get paid extra for your veCRV vote allocations. It’s a blackhole for CRV. Perhaps this sounds familiar if you’ve heard of supply and demand…

Want to dig in deeper on the Flywheel Effects between Curve & Convex? Take a look at Token Brice’s piece (where I borrowed the above two images from) https://tokenbrice.xyz/defi-flywheel/

SUMMARY

Base Curve Flywheel

Capital seeking returns becomes Liquidity in Curve pool

Curve LPs earn half the fees generated by trades, veCRV earns the other 50%

CRV tokens are released as additional yields to LP positions, proportionally

CRV get’s locked for up to 4 years to vote in gauges on how to allocate new CRV

Convex CRV Flywheel

Lock CRV into cvxCRV

Lock that into veCRV

Allocate veCRV votes as directed by vlCVX

Earn CRV and distribute to cvxCRV stakers and vlCVX stakers & lockers

Convex CVX Flywheel

Stake Curve LP positions to Convex for boosted yields through CVX releases

Lock CVX to vlCVX to allocate veCRV to gauges

Earn ‘bribes’ from protocols wanting to have their Curve pool boosts enhanced

Re-stake the earned/paid out tokens to compound yields

Protocol Level Flywheel

Have LP positions on Curve & earn CVX

Offer bribes to have your LP yields boosted

Allocate those CVX to boost your yields & reclaim part of the bribe

Convert protocol LP revenue into Convex positions to enhance future boosts

Votes-As-A-Service Flywheels

Incentivize CVX to be locked up on your protocol

Allocate the represented votes to other protocol pools for a revenue source

Earn more CVX & crvCVX to enhance your power & value to others

Potentially try to beat Convex to other voting services and get a larger market share

This model of irreversible token lockups is proving out to be a highly lucrative model. When things are successful, expect clones! We are now beginning to see the emergence of protocols that offer the exact same model, but instead of attempting to lock up CRV, users can lock up CVX permanently for incentives. The core concept here is essentially that CVX controls the yields of DeFi.

Continue the Convex Finance story here!

Nothing I say should be misconstrued as financial advice. This is all fun and games people.