Making the Flywheels Spin - Convex Finance

Making the Flywheels Spin - Convex Finance

The CVX token, the Convex Protocol, DeFi, and The Curve Wars

Disclaimers!

Change is constant. The numbers I use are based on what I come across at the time of writing - do your own research to evaluate changes in the markets.

I may hold tokens in some of the protocols I discuss.

Nothing in here is financial advice. I’m not your advisor, you need to Do Your Own Research… this is me doing mine. Be careful what you do or you could get rekt! Never share your seed phrase or secret keys, ever!

The blue-chip degen play?

Let’s start with what Convex is, followed by a look at what gives it value right now, then look at the technical ways in which convex could generate revenue in the future - pure speculation abounds here. Next, we will look at what buyers of the CVX token exist, followed by reviewing the financials (and creating those to review) and how to look at the price in how it relates to this aspect.

WHAT IS CONVEX?

To understand Convex, you need to understand DeFi. In simple terms, DeFi is a technology that allows anyone to interact with uncensorable financial instruments at any time. The thing that makes this work is tokenized assets, and the ability to readily swap between one or another of these tokens. Curve is a protocol created to incentivize massive liquidity pools to exist and allow everything else to work as it should. It’s name refers to the curve defining slippage between trading pairs.

How does Convex come into play? Well, there’s this little thing that’s been happening called The Curve Wars, where various protocols want to maximize the incentives their pool(s) receive in the form of CRV tokens. These can either be sold or locked into voting shares to allocate those CRV rewards and earn the trading fees not captured by the Liquidity Providers (depositors into the asset pools). This has become a really big business. With $23 Billion worth of assets in the Curve pools, that boosted yield that can be obtained through votes is massive!

One of the best resources for any protocol is the Docs, so always read through those. Convex’s docs are well done and worth the effort if you’re contemplating getting into this protocol. If you’re technical, reviewing the open source code is one way of protecting yourself.

WHAT IS $CVX?

CVX is the token for the Convex protocol. In it’s plain form of just liquid CVX, it’s just a token. But the power of CVX comes from staking or more importantly, locking it onto the Convex protocol. We will get into the tokenomics of this token further on.

Once the CVX is vote locked, it is the governance token of Convex with the primary goal of directing the votes of Curve’s CRV boosts. The allocation of this source of revenue is a cornerstone of the DeFi ecosystem and has drawn extremely deep liquidity pools. Users who lock their CVX on Convex, they get portions of the revenue generated by the protocol and are also eligible for bribes paid for the allocations of those veCRV votes.

HOW DOES CONVEX GENERATE VALUE?

What attracts people to crypto like moths to a light on a cool summer night? Yields, right? The old saying goes “come for the yields, stay for the ____” (fill in the blank with whatever you personally find valuable about crypto/defi). Well, the backbone of the entire ecosystem is the ability to move your money instantly from one asset to another and that requires massive amounts of liquidity. And where do you find the absolute deepest liquidity for many important stable pairs (and now with v2, some not as stable pairs)? You go to Curve, even if you don’t know you’re going to Curve.

Before proceeding, it might be worth understanding what the flow of tokens from Curve & Convex looks like. I’d recommend taking a look at another, short piece:

The Value Proposition

What drives the value of the $CVX token?

There are two main sources of value generation for CVX: Cashflow & Increased Demand. Some of the ways in which cashflow is created for CVX holders is earning a cut of the Convex’s CRV revenue, getting paid bribes for allocating your CVX votes to pools offering bribes (see Votium), and as we discussed, boosting the yields for pools you have a LP position in (can be compounded through staking LP on Convex).

Bribes

Bribes are a recent development in the space, having completed 8 rounds of CVX bribes through Votium, we have seen a rapid growth in just how much protocols are willing to pay to buy curve pool gauge weight votes. As it sits currently after round 8, the cap of total votes was raised to 50% of all of Convex’s veCRV votes (now even that 50% cap has been removed). The bribe amounts have been roughly increasing by double each round, reaching just shy of $1 per vlCVX through Votium’s interface. This is supplemented by the bribe.curve.finance platform, where if you delegate to a pool offering bribes only to veCRV votes, you get those rewards as well. These are currently smaller amounts, but still a very real source of yield.

The value of a single vlCVX vote is variable, based upon the yields it can generate, which determines how much a protocol can pay for those votes. It’s also influenced by how many votes a single vlCVX controls, which changes as the number locked and participating varies, as well has by how many CRV have been locked in Convex. Don’t worry, I’ll discuss this in greater detail down below!

This article linked here discusses how the bribes work in detail. Keep in mind that this was specifically created for veCRV gauge votes, while the main source of bribes for vlCVX has become Votium. You still can get the bribes from this as well. https://andrecronje.medium.com/bribing-vecrv-gauges-101-8f6e4506bb62

When CVX is vote locked for ~16 weeks (vlCVX), the owner is able to receive bribes from protocols looking to boost their Curve LP’s CRV yields. The bribe superstore for vlCVX is available through a project called Votium, where protocols can offer up sums of tokens and hope that people allocate their vote weights to them. The vlCVX holders are able to either delegate their weight to Convex or Votium to be allocated as they see fit, or select a specific bribe to allocate to. If you delegated and forget to cast your vote, Votium will spread the votes out in attempt to equalize the yields across all bribes. The imbalance exists becauses users may only want to receive a single specific token, tending towards an over-allocation to the CVX token bribes to maximize CVX holdings… to lock on Convex, to claim more bribes on, to boost yields & generate more CRV, to lock up… See? Flywheels everywhere!)

Additionally, this method of pooled vote casting improves gas efficiency in multiple regards. You can vote for a single token to reduce claiming expenses (or maximize yields if planning to sell tokens off). It also reduces the number of CRV to veCRV locks, gauge weighting votes, and claims, which is beneficial for Ethereum at large by reducing the consumption of blockspace! The variation in yields can be significant even within a single round. For example, in Round 8, the difference between the highest yield bribe and lowest yield bribe was $0.97 per vlCVX vote for FXS (Frax) rewards vs. $0.72 per vote for CVX rewards. Or if a user doesn’t care what they get, Votium can balance out the unallocated votes across all pools to maximize yields and cost bribe cost-efficiency for protocols.

The Future of Bribes

It is all determined by the tokenomics of the flywheel: number of votes controlled per CVX, the $ value of the CRV emissions, the number of CVX eligible for the bribes vs. not locked but instead in Curve liquidity pool pairs. Don’t forget that the total CVX supply is 100M of which 80.8M have already been minted. Based on the mechanism for the issuance that we will discuss in the linked article below, the issuance rate may be beginning to drop off quickly from where we are right now.

The tokenomics of the CVX & CRV relationship is discussed in a side article I wrote. I highly recommend taking a look at this before proceeding.

Now that we better understand how & why CVX get’s printed, let’s see how the supply and demand forces work in a free market system.

Vote-o-nomics

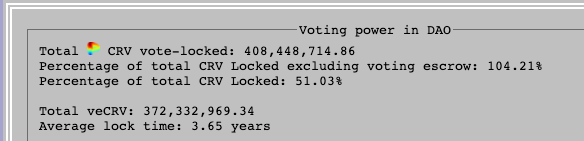

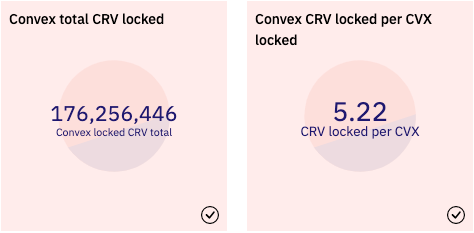

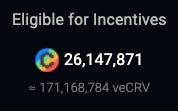

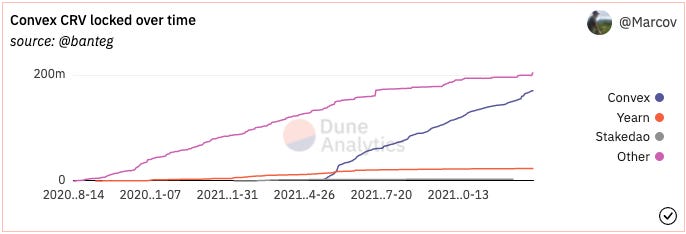

The voting power that Convex wields is based upon the number of CRV held and locked into veCRV. Currently, Convex controls 176M veCRV out of the total 372M, or 47.3%. Note that there’s fewer veCRV than vote-locked CRV. This is because the duration of the remaining portion of the lock is important: 4 year lockup is 1 veCRV per CRV, diminishing all the way to unlocked CRV which has 0 votes.

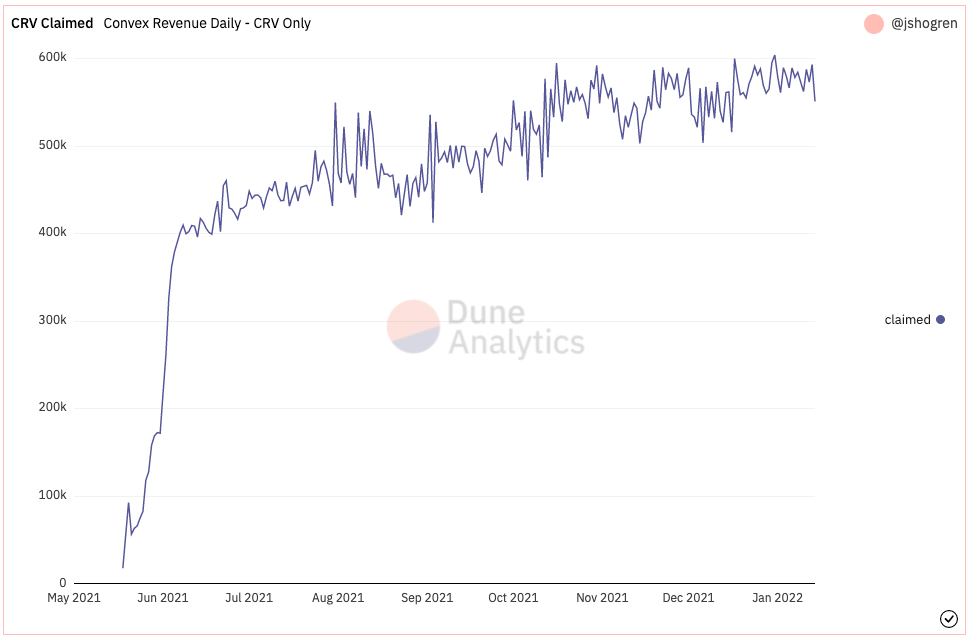

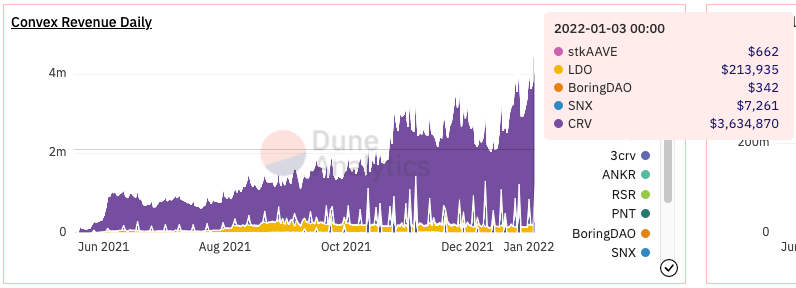

Between the increasing LP The number of CRV Convex claims per day has grown from 400k in mid-June 2021 and is now about 600k early-Jan 2022.

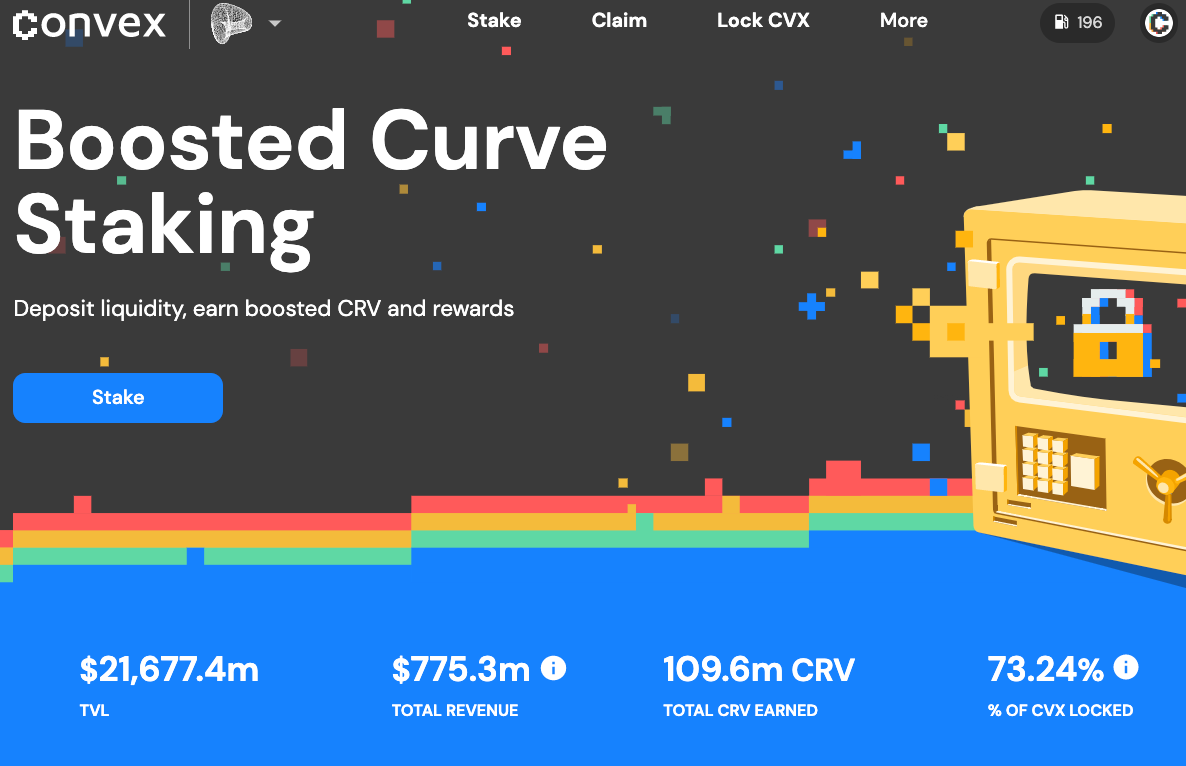

To be eligible for the bribes and protocol fees, CVX must be vote locked for 16 weeks. You have the option to delegate your votes to wherever you’d like, but Votium has become the standard since they created the CVX bribe platform, collecting 4% of the bribe upon creation. Currently, 73.24% of the current circulating CVX is locked into vlCVX. Of those, 30.5M* are eligible for the bribes.

* Update for round 9: 30.5M CVX eligible, 14.5M delegated to Votium

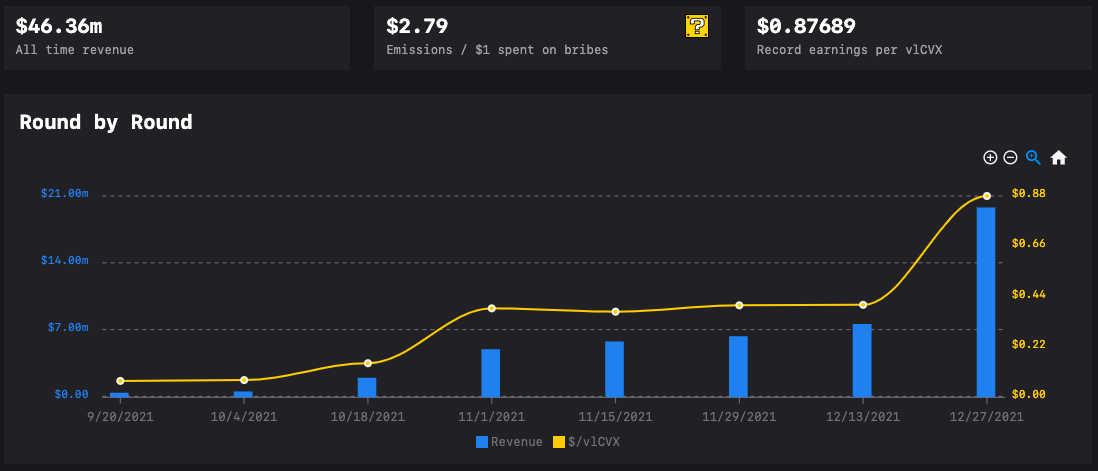

Currently, the bribers increase their Curve Pool yields by $2.79 per $1 they spend on bribes (please note that the values shift as things are finalized, and the final $ value may not be the same as when the round closed as token prices change).

So, all that being said, what the heck does it mean? Well, that’s where your risk tolerance and assumptions come into play when looking at this.

Increased Demand - Profits & Competition

I’m going to make a pretty big assumption and assume that market forces will drive everyone to maximize profit and maximize competition.

What do I mean? Everyone who can make money on this will do so and that profitability will be maximized: that bribe yields will be bid down (by paying more, think: bonds) until they’re almost at break-even. Of course, the bidders get to stack CVX as part of the yields along the way (see how Frax has simply staked the protocol’s Curve LP and built up a massive amount of CVX).

The $ amounts of the bribes still have room to increase substantially while keeping it profitable for the protocol and enhancing the bribe payouts. This is tracked nicely on Votium. Currently, for every $1 spent on bribes, the CRV emissions boost is increased by $2.79! That’s a deal, and a massive opportunity for arbitrage.

The number of CVX claiming the bribes can increase dramatically. Currently, only 30.5M CVX are eligible for the bribes by being locked on Convex into vlCVX, but theoretically every single CVX could be eligible. However, you must factor in that there are CVX in Liquidity Pools earning similar $ yields and not everyone is comfortable with locking up a token for 16 weeks. The number getting bribes vs. earning yields will likely be a dynamic interplay between these (and other) factors and may end up finding some sort of equilibrium.

You might be thinking that “this all seems so good to be true” or “yeah, but what’s the cost of using this type of a platform” and that would be a smart question to ask. Before we get into the yields paid out to the users, let’s take a quick look at fees associated with using these services, and what that actually means for us.

Fees? Yes please!

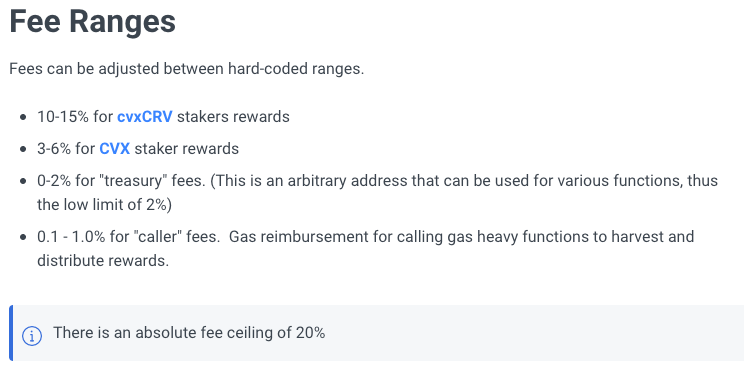

Convex’s revenue comes from taking a performance fee off the generated CRV issued to the Curve LPs (see The Flywheel discussed above). Convex currently takes 17% of the CRV generated by staked LP positions, distributing the revenue to cvxCRV stakers (10%), CVX stakers & lockers (5%) & CVX lockers (bonus 1%). The protocol also takes a portion to fund operations, developers, gas expenses, etc.

From Convex’s documentation regarding fees:

The “revenue” shown here isn’t what Convex is taking in fees, but it is the amount being generated by the end user positions. The fees are deducted from these amounts.

One other fee is through Votium, where they take 4% of the bribe when it’s created. This reduces the entirety of the bribe pool available and is not taken from just Votium delegators. This feels super reasonable since vlCVX allocators still get large payout on a bi-weekly schedule. Let’s all thank the Votium team for building awesome!

All these fees may feel disappointing at first glance, taken from the yields being generated by the LP positions staked onto the protocol. Gimme that back it’s mine! Well don’t cry anon, you do get it back! The fees are the base method for CRV to be captured and retained by Convex. This grows the voting power of the vlCVX and is completely relevant to the entire flywheel we’ve been discussing. Although users can also permanently lock up the CRV into cvxCRV (that’s a 3) and re-lock the yields (another 3). Then stake/lock it all (3,3) for sure!

But wait, you said the fees would be good?! That 3,3 action I just mentioned? That’s you getting your fees back to you as cvxCRV after the protocol retains it’s portion. These tokens swappable in a deep LP pool, but cvxCRV is a perma-locked veCRV that retains liquidity. Yep, you get paid a yield in 3crv, essentially a stablecoin. This is crypto, it’s a win-win-win-win all around!

Maximal Profit Making - An Equilibrium TBD

Not every CVX will end up staked. There are many ways this token can likely be used, but I’ll focus on just the two that currently exist. Right now, owning CVX get’s you approximately a 60% yield annualized, regardless of whether it is $ value in either of the LP pools cvx/eth or crv/eth on Curve (sushiswap’s pool is being phased out with no new yields allocated to it).

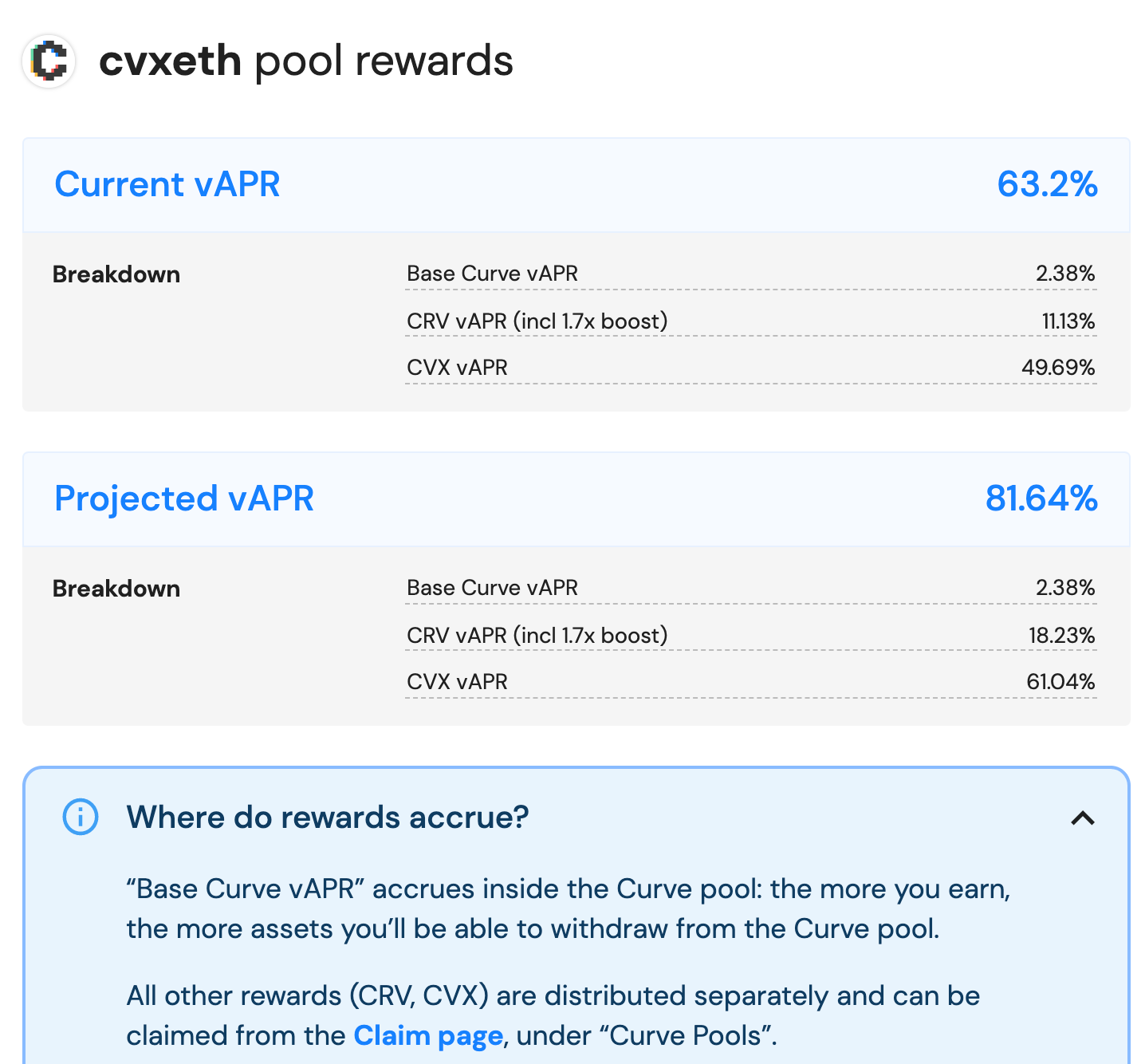

The other option is vote locking it for 16 weeks and earning the bribes. Currently $1 per cvx vote is $26 per year per token. At a price of $45, that’s 58% APR, plus the 4% earned as protocol fees paid in cvxCRV, so 62%. The yield for staking in the cvxeth pool is 63%. Maybe add in 1% more for the other veCRV bribes you may get? Seems like you’d need to decide what your own preference is if you took a position…

Let’s take a look at the yields for these various positions one could take, and how those are broken down.

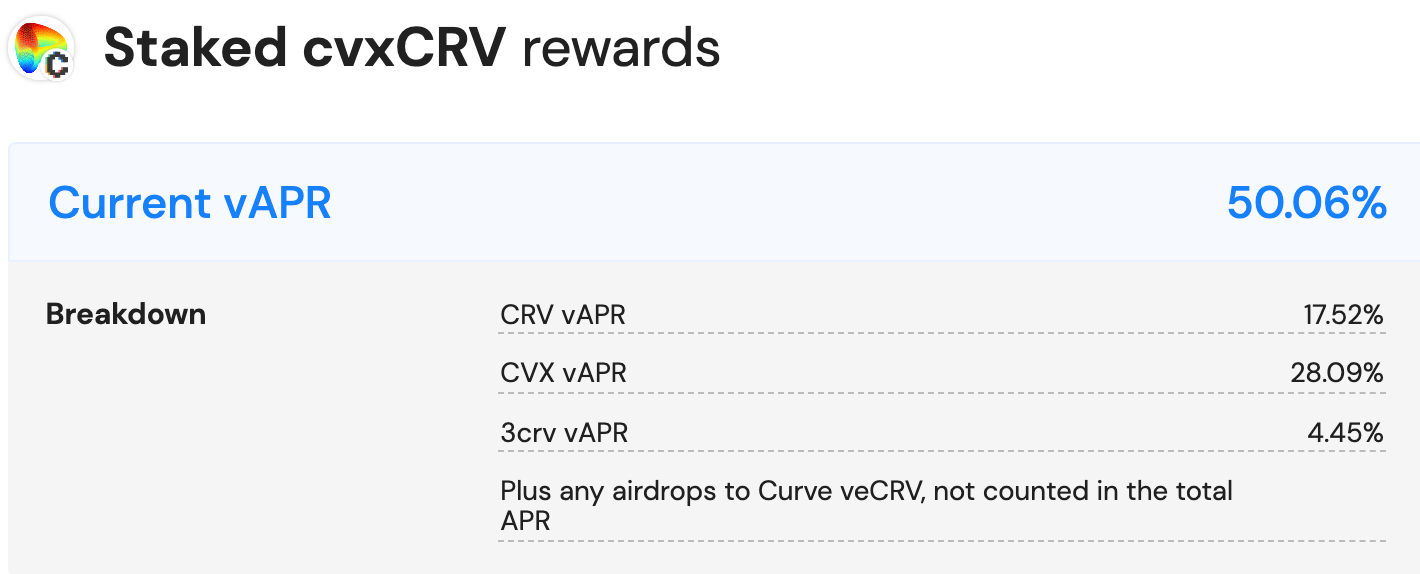

The cvxCRV generated by your vlCVX or if you directly lock base CRV in, and can be claimed & re-aped, paying a nice additional compounding:

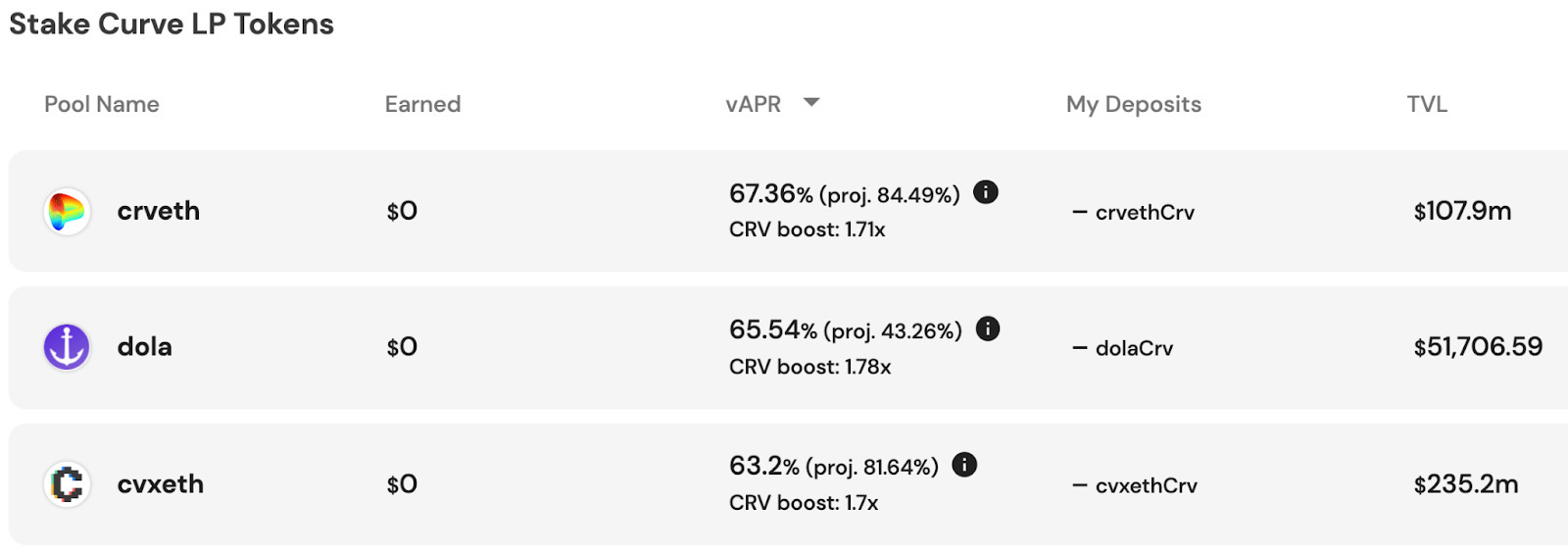

If you want to be liquid an maximize yield, being a Liquidity Provider on Curve and staking to Convex pays healthy yields:

These LP position returns are broken down as shown, but are subject to change based upon the rate of CRV captured (the boosts being voted on with vlCVX) as well as the allocation of the MasterChef contract (the other 25% of all CVX being allocated to incentivize positions over a 4 year period).

As mentioned before, there are tradeoffs for both strategies. If you’re an LP, you’re only 50% exposed to the price appreciation of either CVX or ETH, but susceptible to both, as we know it, Impermanent Loss. But if you’re bullish on both, you can consider being an LP incentivized Dollar Cost Averaging into the lesser performing asset. Maybe that’s good, maybe that’s bad, but it’s definitely not financial advice. Either way, you’re stacking up crvCVX & CVX along the way and as it was discussed in the tokenomics section, time is of the essence with the rate of CVX minting down to the last 19% or so!

If you don’t like impermanent loss, you can lock your CVX, but you then no longer have liquidity to take profits if CVX runs up. You also then either need to manage your vote every 2 weeks or be ok with however Votium allocates your votes, which will likely maximize $ yield, but leave you with many tokens to claim; not a big deal if you’ve got big bags and you cannot lie…

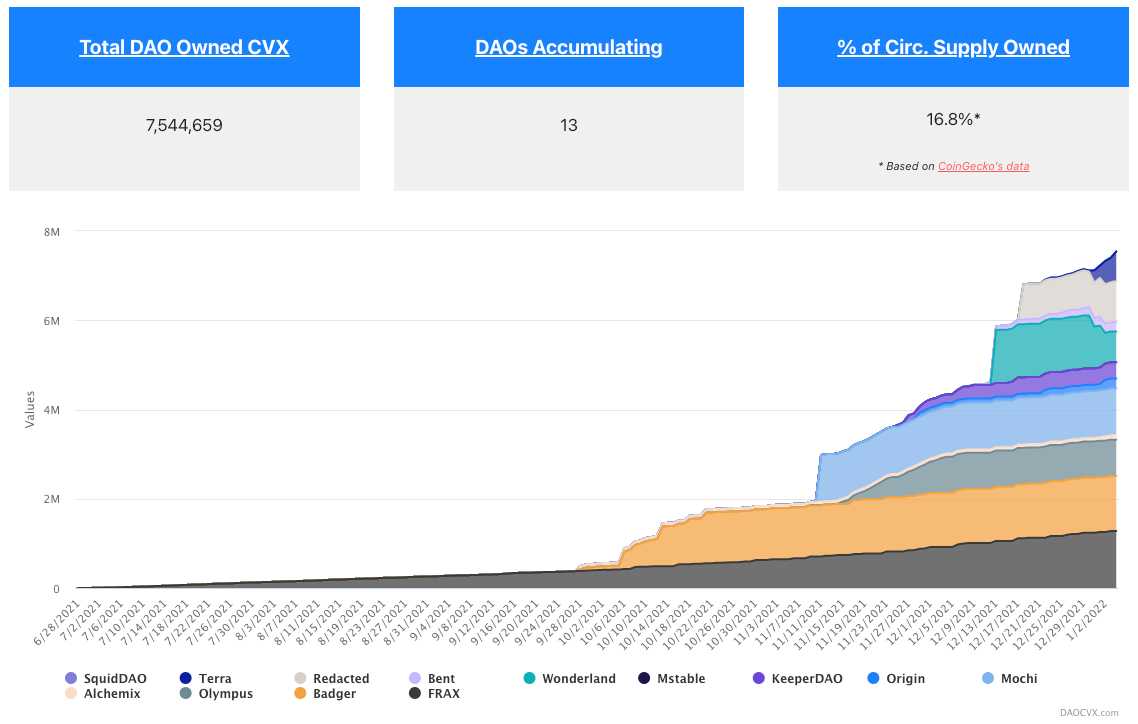

Maximal Competition - Buyers of CVX

Remember way way up above where we talked about The Flywheel? Well, there are multiple layers to that flywheel. Curve has it’s own with the creation of crv and the locking up of said tokens. Convex created a second layer where lockups happen and new tokens are issued. And, just like anything innovative/incredible/paradigm-changing in DeFi, when something works, emulate it! Now there are more layers building up on top of what Convex has done. Sure, they’re now competing for CRV, but with Convex’s significant lead, there’s no way to catch up, just lock in market share. To get around that, these new protocols are allowing users to lock up CVX tokens irreversibly… if you can’t join ‘em, own ‘em? Additionally, the protocols paying those bribes that bring us so much joy are stacking CVX and even buying more. Let’s take a look at some examples of CVX Blackholes.

Redacted Cartel

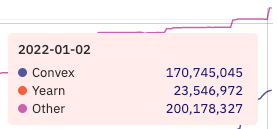

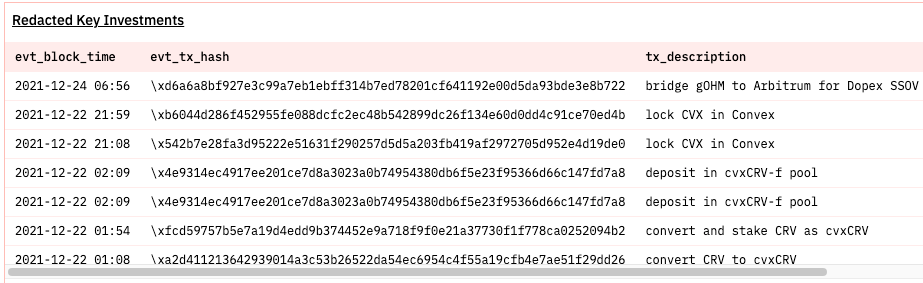

Having control of your protocol’s liquidity has proven its self to be a key piece of the DeFi infrastructure. What about having absolute control over the income generated by that mountainous bag of liquidity you own? Well, this whole new ecosystem is becoming known as ve-aaS, or vote-escrow as a service, what I like to call GovFi. Just as Olympus DAO revolutionized the game with their bonds, well there’s a new kid on the block, [REDACTED] Cartel.

By utilizing the forced growth caused by rebase tokenenomics, [REDACTED] plans to Hoover up yield bearing governance tokens as the Treasury Collateral of their $BTRFLY token. In fact, just today while I was writing this up, I noticed that their treasury began it’s first rounds of purchasing, buying up $45M of CVX and $39M of CRV. What’d they do with it? Locked it up into Convex.

Here you can see the Convex locks. Look way out at today… That’s [REDACTED] in action.

Before the buy… After the buy…

Annnnnd Locked!

Bent Finance

Another blackhole for CVX where you lock the CVX up for a yield in Bent. Currently this is sitting at 213.62% APR on your CVX locked. It’s an irreversible lockup. This protocol has experienced some hacks in the past so be careful!

Curvance - tbd?

Making a play off lending against the stablecoin LP pools and lockups. Yields will abound! Keep an eye out for updates on their website.

Bribe Protocol

Get paid for any governance token vote? The possibilities are endless! Link to their site.

Other Buyers

Alchemix, Abracadabra, BadgerDAO, StakeDAO, Frax, and many more are paying for bribes. They then get to accumulate CVX as rewards and or take that profit and buy up CVX. So there are a lot of well-endowed buyers out there who would be extremely unlikely to sell since this is how the protocol generates revenue.

Ok, well that’s a wrap. Yeah, just kidding! We’ve scratched the surface of how the flywheel spins in the Curve Wars, and the potential financial implications arising from that for holders of CVX. Keep an eye out for the next part of the story where we will look into potential growth opportunities for Convex and therefore the potential value that creates!

Stay safe out there!

RISKS & DISCLAIMERS

This was not paid content.

I’m not telling or suggesting that you do anything with your money.

Do your own research!

I’m not your advisor.

I’m not your mom.

I own CVX.

I’m just another smooth-brained ape out here in the wild.

Don’t share your seed phrase or private keys with anyone, ever!

I certainly will NEVER ask for them.

Understand what people mean when they say “there’s always contract risk” because that is really, actually, not a joke - hacks happen often and can be devastating.

Also, understand what regulatory risk means and consider it - we are on the bleeding edge of the decentralized economy, and anything can happen.